Why Growing Your Medical Practice Doesn’t Always Build Wealth

Most physician owners know whether last year was a good year. Collections were up. Revenue increased. Maybe a new provider joined the practice. Maybe patient demand remained strong despite all the challenges facing healthcare. By most measures, the practice was … Read more…

Jeff Bourdage: Trusted Advisor, Teacher at Heart, and Humble Champion for Small Business

Celebrating the legacy of a partner who built lifelong client relationships, helped shape a growing firm, and embodied the people-first spirit of Jones & Roth. A Career That Started with Family — and a Promise Not to Marry an Accountant … Read more…

401(k) Catch Up Contributions Are Changing in 2026: What You Need to Know

Significant changes are coming in 2026 for high earning workers who make 401(k) catch‑up contributions to their employer retirement plans. These updates, which were created under the SECURE 2.0 Act of 2022, continue a broader legislative trend that encourages the … Read more…

6 ways contractors can better manage accounts receivable

Aging accounts receivable can hurt any construction business’s financial performance. And as you’ve probably experienced, it’s a common issue. Payments are often delayed by last-minute change orders, hefty retainage, project disputes and slow approvals. Here are six ways to better … Read more…

Jones & Roth Reflects on a Successful 2026 Pacific Northwest Healthcare Leaders Conference

Jones & Roth CPAs & Business Advisors was proud to serve as a sponsor and exhibitor at the 2026 Pacific Northwest Healthcare Leaders Conference, held May 20–22 at the Hilton Vancouver Washington in Vancouver, Washington. The conference brought together healthcare … Read more…

David (Dave) Gault: A Three‑Chapter Career of Service, Leadership, and Quiet Mastery

Celebrating the legacy of a professional whose five‑decade career shaped clients, colleagues, and communities across Oregon. Early Years and the Path Toward Accounting When Dave Gault graduated from Medford High School in 1956, he left with a perfect 4.0 GPA … Read more…

Nonprofit Donations: Donor Acknowledgment

Donations are essential to non-profit organizations. Non-profit organizations should establish policies and procedures for acknowledging charitable contributions. Proper donor acknowledgments not only help donors substantiate tax deductions but also demonstrate good stewardship and donor service. When donors make a single … Read more…

What’s in a name? DBA filings for construction businesses

The name of your construction business plays a critical role. It helps project owners find, recognize and ultimately trust you. But as your business grows, you may encounter situations where a different name better suits your strategic objective. Whether you’re … Read more…

EV Plug-in Credit Set to Expire on June 30, 2026: Have You Claimed Your Credit?

A looming deadline is coming for anyone thinking about adding a charging station to their personal residence or for their dental practice. As we see electric vehicles become more and more popular on the roadways, charging stations will soon gravitate … Read more…

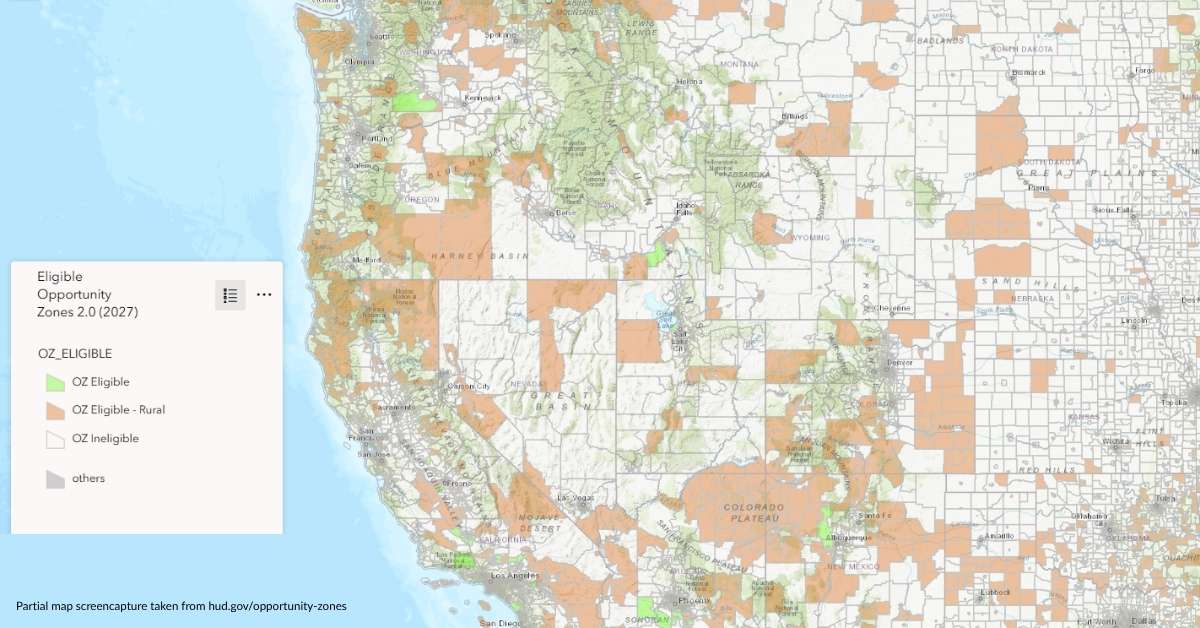

Maximizing Tax Efficiency Through Qualified Opportunity Zone Investments: A Strategic Perspective from Your CPA Advisors

As tax professionals, we know that effective investing is about more than market performance — it’s about structuring your financial decisions to minimize tax exposure and maximize long‑term value. Qualified Opportunity Zone (QOZ) investments may offer certain tax advantages for … Read more…

Mid-Year Planning: Benchmarking for Healthcare Practices

Benchmarking key performance indicators has become essential for healthcare practices that want to stay competitive, financially resilient, and patient centered. As the industry faces rising costs, shifting regulations, and increasing patient expectations, leaders cannot rely on intuition alone to guide … Read more…

Oregon’s Pass Through Entity Tax (OR PTE) Is Back: What You Need to Know for 2026

Oregon’s elective Pass‑Through Entity Tax (OR‑PTE) is officially back for the 2026 tax year, thanks to the passage of SB 1510. The bill extends the OR‑PTE program through 2027 and clarifies how overpayments can be applied to future estimated payments. … Read more…

4 Reasons Contractors Should Exceed Safety Expectations

Running a construction business requires compliance with the Occupational Safety and Health Administration’s (OSHA’s) many rules. But there can be a big difference between doing the bare minimum and building a robust safety culture that goes beyond basic requirements. Along … Read more…

Navigating Rising Healthcare Costs: Highlights from Our Alliant Webinar

Jones & Roth CPAs was honored to host a recent webinar featuring Shelli Littlefield, REBV, RHU, ChHC, Vice President at Alliant Insurance Services, who delivered an insightful and timely presentation on the rapidly changing world of healthcare benefits, cost containment … Read more…

Tax Brief: Form 990 – Breaking Down the Statement of Revenue

Form 990, Part VIII, Statement of Revenue reports revenue by type and classification of revenue and is one of the most important parts of the Form 990. Breakdown of Types of Revenue Types of revenue include Contributions, Gifts, Grants, and … Read more…

Tempting targets: Contractors and cybersecurity

You might think your business is too “small potatoes” for cybercriminals to bother with, but that could prove costly. Construction businesses of all sizes make tempting targets for various reasons — not the least of which is that many contractors … Read more…

IRS Notice CP53E Causing Confusion for Taxpayers

The IRS has recently caused widespread confusion by issuing Notice CP53E to a broad range of taxpayers, many of whom were not expecting a refund. The notice requests bank account information so the IRS can issue a direct deposit, but … Read more…

Event Recap: Top 10 Ways to Recession-Proof Your Practice

The evening of May 7th, we had the pleasure of hosting our Client Appreciation Evening at Harder Day Café in Lake Oswego alongside our partners at Columbia Bank Healthcare. It was a great opportunity to spend time with our healthcare … Read more…

When Tax Strategy Meets Life Strategy: Why CPAs and Investment Advisors Must Work Side by Side

Most people experience their financial lives in fragments. Taxes are handled by one professional. Investments by another. Retirement planning sits in a separate silo. Estate planning lives in yet another binder, often unopened. Each advisor may be competent, even excellent, … Read more…

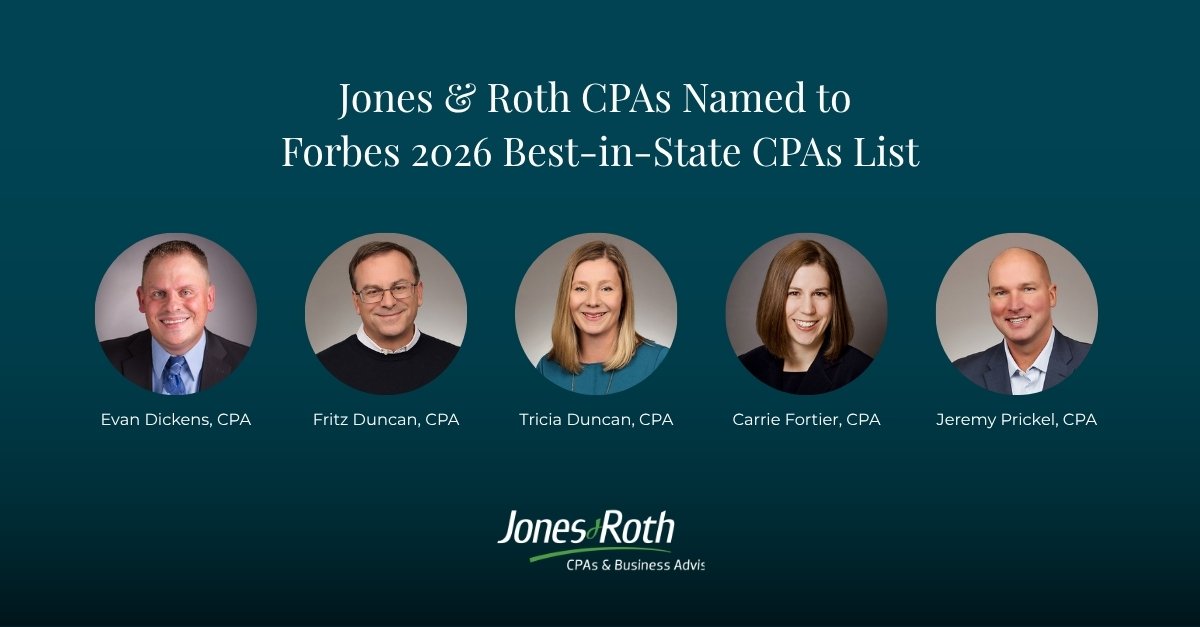

Jones & Roth CPAs Named to Forbes 2026 Best-in-State CPAs List

Jones & Roth is proud to announce that five Team Members have been named to the Forbes 2026 Best‑in‑State CPAs List, a prestigious national recognition honoring top Certified Public Accountants who demonstrate excellence in their profession, exceptional client service, and meaningful contributions to the accounting industry. The Jones … Read more…

Nonprofit’s Guide to Financial Statement Services: Audit, Review, Compilation, and Preparation Services

Financial statements are a critical tool used by management and boards of nonprofit organizations to gauge how well the organization is performing, determine the strength of financial position, and make informed decisions for the future of the organization. Financial statements … Read more…

Where to find the Jones & Roth Healthcare Advisors: Upcoming events you won’t want to miss

Spring is shaping up to be a busy and energizing season for our team — and we’d love for you to be part of it. We’re going to be popping up at in‑person learning events, virtual sessions, or opportunities to … Read more…

The Dental Practice Life Cycle: Navigating the Purchase and Early Growth Years

Purchasing or starting a dental practice is one of the most rewarding steps in a dentist’s career and one of the most demanding. Almost overnight, clinical responsibilities are joined by the realities of ownership: managing cash flow, overseeing staff, making … Read more…

The S-Corp Hype: What Social Media Isn’t Telling You

Thinking About an S-Corp for Your Medical Practice? Here’s What You Need to Know Scroll through Instagram or LinkedIn and you’ll see it everywhere: “Form an S-Corp and save thousands in taxes!” Influencers make it sound like the ultimate business … Read more…

6 steps to an incentive compensation program for contractors

Is your construction company struggling to attract and retain quality workers in today’s tight labor market? A well-designed incentive compensation program may help. The right approach can increase productivity and profitability while boosting employee satisfaction and company culture. However, you’ve … Read more…

The Evolving Landscape of Healthcare Benefits and Insurance Strategy

Scroll down for the replay video. Webinar: Thursday, May 8 | 12:00–1:00 PM Healthcare practices are navigating a challenging benefits environment. Rising insurance costs, competitive labor markets, and growing employee expectations are forcing practices to rethink how they design and … Read more…

Tax Brief: Form 990, Schedule B: Schedule of Contributors

The purpose of Schedule B Schedule of Contributors in the Form 990 is to report information on contributions the organization recorded during the tax year. The IRS utilizes Schedule B information to match donors’ tax deductions to the organizations they … Read more…

Is Your Healthcare Practice at Risk for Fraud? Here’s What You Need to Know

Fraud isn’t just a big-business problem — it’s a growing concern for healthcare practices of all sizes. Whether you run a solo clinic or manage a multi-provider group, your practice may be more vulnerable than you think. Rising operational costs … Read more…

Jerry Willey: Builder, Bridge Maker, and Champion for Community and Clients

Celebrating the legacy of a partner whose leadership shaped Jones & Roth and whose public service strengthened an entire region. A Northwest Beginning — and a Partnership That Endured Jerry Willey’s career began in Walla Walla, Washington, where he entered … Read more…

Utilizing the Power of QR Codes for Non-Profit Organizations

In the New Media Age, non-profit organizations face increasing challenges when it comes to engaging with donors, volunteers, and beneficiaries. To overcome these obstacles, many non-profits are turning to innovative technologies such as QR codes (Quick Response Codes) to enhance … Read more…

Why Dentists Should Raise Their Fees in 2026: A CPA’s Perspective

Let me share a story I hear all the time from dental clients. A dentist calls me in frustration: “I’m working harder than ever, but my profits keep shrinking. Where is all the money going?” After reviewing their numbers, the … Read more…

Understanding Phantom Income: The Hidden Tax Impact of Section 179 and Bonus Depreciation for Medical Professionals

As a medical professional, you understand that keeping your practice equipped with the latest technology and equipment is essential for providing high-quality patient care. Whether you’re upgrading diagnostic tools, purchasing new medical devices, or improving your office setup, these investments … Read more…

How to run a leaner, more profitable construction business

Lean construction principles focus on reducing waste, improving workflow and making better use of key resources such as labor, materials and equipment. And you don’t necessarily have to undertake a complete operational overhaul to implement them. By identifying and correcting … Read more…

The Next Step in Protecting Your Wealth

As a doctor, you’ve worked tirelessly to build a thriving practice and with it, meaningful wealth. But creating wealth is only the beginning. The true measure of success is ensuring that it endures, safeguarding your family’s future for generations while … Read more…

Robin Matthews: Innovator, Mentor, and Champion for People and Possibilities

Celebrating the legacy of a partner who transformed services, shaped leaders, and expanded what was possible at Jones & Roth. A Unique Path Fueled by Curiosity, Courage, and Growth Robin Matthews’ career at Jones & Roth began in a way … Read more…

Key 2026 Employment Law Updates Healthcare Practices Must Prepare For: Insights from Watkinson Laird Rubenstein

Thank you to Daniel K. Olson, J.D. and Jaclyn K. Rudebeck, J.D. of Watkinson Laird Rubenstein, P.C. for an incisive update tailored to healthcare practices. The presentation covered a compact but consequential agenda — noncompetition agreements, the new overtime pay … Read more…

Oregon SB 1510A Extends PTE-E Through 2027

Dear Clients, Oregon’s 2026 legislative session delivered significant news for pass through business owners. SB 1510A, now passed by both chambers and awaiting the Governor’s signature, includes a highly anticipated provision: the extension of Oregon’s Pass-Through Entity Elective Tax (PTE-E) … Read more…

Jill Foster: Trailblazer, Mentor, and Champion for Clients and Community

Celebrating the legacy of a partner who shaped Jones & Roth and expanded what was possible for women in the profession. A Non-Traditional Path with Extraordinary Impact Jill Foster’s journey to Jones & Roth wasn’t linear — it was bold, … Read more…

The Smart Dentist’s Guide to Entity Selection: Protect Your Practice and Maximize Tax Savings

Your dental expertise creates healthy smiles, now let the right business structure create financial security. Choosing the proper entity can save you thousands in taxes and safeguard your assets, but navigating these decisions isn’t something you should tackle alone. Partner … Read more…

Employment Law Updates for 2026 – Upcoming Webinar for Healthcare Practices

Staying current with employment law is essential for healthcare practices navigating an evolving regulatory environment. On February 27, the Jones & Roth Healthcare Advisors hosted an informative online presentation covering the most important Oregon employment law updates and trends impacting … Read more…

Uniform Guidance: De Minimis Indirect Cost Rate

The Office of Management and Budget’s (OMB) Uniform Guidance (UG) makes available the use of the de minimis indirect cost rate to allow not-for-profit (NFP) organizations that do not have a current Federal negotiated indirect cost rate to have at … Read more…

No Extension in Sight: Oregon PTE-E to End After 2025

Update: See our 3/5/26 post: “Oregon SB 1510A Extends PTE-E Through 2027” As of February 9, 2026, Oregon’s Pass‑Through Entity Elective Tax (PTE‑E) is still scheduled to sunset for tax years beginning before January 1, 2026. Despite ongoing interest from … Read more…

Jones & Roth’s Legacy of Independence: 80 Years Rooted in Oregon

1946 was an important year in the history of our world. In January 1946, the United Nations was founded in London. In June 1946, the National Basketball Association was formed in New York. In December 1946, the timeless holiday movie … Read more…

Webinar Replay: What Every Nonprofit Needs to Know About Form 990

Jones & Roth’s Nonprofit Team is excited to present a webinar designed to help nonprofit leaders navigate an important IRS filing: Form 990. This form is more than just a compliance requirement—it’s a critical document that can influence how donors … Read more…

SECURE Act 2.0: What Doctors Need to Know About the 2026 Retirement Plan Changes — A Tax & Compliance Update

As your CPA advisors, we understand that doctors face unique financial pressures — from managing a demanding clinical schedule to overseeing the business side of a medical or dental practice. Retirement planning is a critical part of protecting your long‑term … Read more…

Tax Brief: Board Review of the Form 990

The IRS requires nonprofit organizations to disclose whether the Form 990 was provided to all members of the Board of Directors prior to filing and to describe the review process used. Board review of the Form 990 is not statutorily … Read more…

Trusts & Estates and the new mandate for electronic payments–what do you do?

On March 25, 2025, President Donald Trump issued Executive Order 14247, mandating that all federal payments — including tax payments to the IRS — be made via electronic funds transfer (EFT). This directive is part of a broader initiative to … Read more…

Five Tips for Making Your Nonprofit’s Financial Statement Audit Stress-Free

For many nonprofit leaders, the annual financial statement audit feels like a necessary headache—time-consuming, stressful, and disruptive. But it doesn’t have to be that way. When managed well, an audit is more than a compliance exercise; it’s an opportunity to … Read more…

2026 Dental Industry Outlook: How Practices Can Thrive Amid Change

As we enter 2026, the dental industry faces a critical turning point. Economic uncertainty, evolving patient expectations, workforce challenges, and rising operational costs are reshaping the business landscape for dental practice owners. Success this year will require more than optimism, … Read more…

Join Us at the Oregon MGMA 2026 Grants Pass Summit

We’re excited to announce that Keegan O’Brien, CPA will be speaking at the Oregon MGMA 2026 Grants Pass Summit on Thursday, January 15, 2026, from 12:00 PM – 4:00 PM PT at AllCare Health, 1701 NE 7th St, Grants Pass, … Read more…